Deciding whether to rent or buy in Jupiter, Florida, has never been a simple lifestyle choice.

It’s a financial decision layered with insurance costs, HOA fees, interest rates, and the unique pressure of a seasonal market that behaves very differently from most of the country.

What worked here five or ten years ago doesn’t automatically hold up today.

Jupiter continues to attract buyers and renters thanks to its beaches, boating lifestyle, strong school zones, and proximity to major employers like Jupiter Medical Center, Scripps Research, and Roger Dean Stadium.

But with rising ownership costs and limited inventory, many residents are pausing to do the math instead of jumping into the market.

In this guide, we’ll break down the real numbers behind renting versus owning, explain where each option makes sense, and walk through neighborhood-specific examples so you can make a decision based on facts—not headlines—when weighing rent vs buy Jupiter FL 2026.

Is It Better to Rent or Buy in Jupiter, FL in 2026?

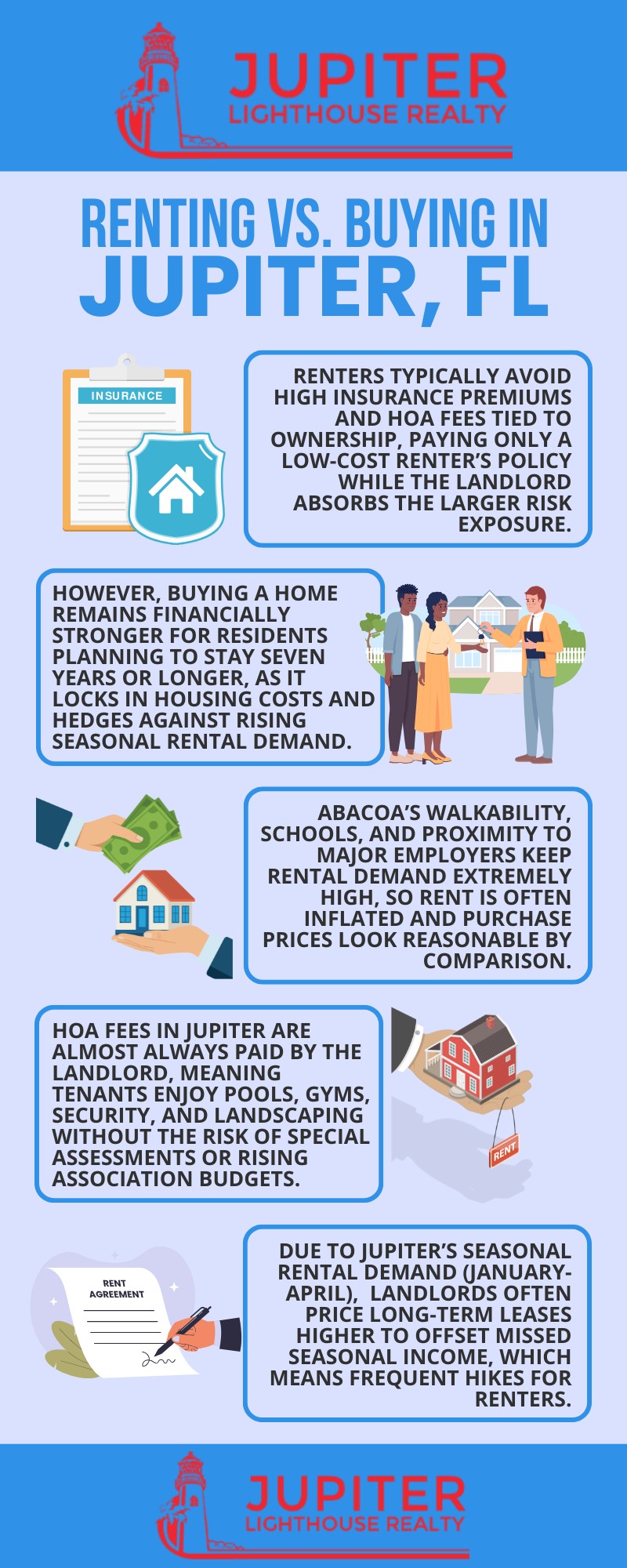

In 2026, renting in Jupiter is usually cheaper month-to-month due to high insurance premiums and HOA fees tied to ownership.

Buying, however, remains financially stronger for residents planning to stay seven years or longer, as it locks in housing costs and hedges against rising seasonal rental demand.

The key isn’t just cost—it’s timeframe.

Is It Cheaper to Rent or Buy in Jupiter, FL in 2026?

The Monthly Math

Break-even horizon: approximately 5–7 years in Jupiter.

This longer break-even window is driven by:

- High closing costs in Florida (often 6–8% round-trip)

- Elevated insurance premiums

- HOA fees that don’t build equity

For most buyers, it takes at least five years of ownership before appreciation and principal paydown begin to outweigh upfront costs.

Upfront Capital

Buying requires significantly more liquidity than renting.

Buying (typical condo):

- Down payment: 5–20%

- Closing costs: 2–4%

- Prepaids (insurance, taxes): several months upfront

Renting:

- First month’s rent

- Last month’s rent

- Security deposit

For a first-time home buyer, Florida 2026, this gap alone can delay ownership—even when monthly income supports a mortgage payment.

How Jupiter FL Homeowners Insurance Rates Impact Buying

The Hidden Mortgage Cost

One of the biggest shifts in Jupiter FL housing affordability in 2026 is insurance. Homeowners insurance is no longer a background expense—it’s often the deciding factor in loan approval.

Unlike rent, insurance premiums:

- Can increase annually

- Are factored into your debt-to-income ratio

- Directly reduces buying power

Many buyers are approved based on today’s rate, only to feel squeezed when premiums reset.

Wind vs Flood

In coastal and near-coastal zones, most owners must carry:

- Windstorm coverage

- Flood insurance

Renters typically avoid this burden, paying only a low-cost renter’s policy while the landlord absorbs the larger risk exposure.

Abacoa Rentals vs Sales: Which Is the Better Move?

Neighborhood Case Study

When comparing Abacoa rentals vs sales, the math often surprises people.

Abacoa’s walkability, events, schools, and proximity to major employers keep rental demand extremely high. As a result:

- Rents for townhomes and condos are often inflated

- Purchase prices can look reasonable by comparison

For buyers who can manage the HOA fees, owning a townhouse in Abacoa can be competitive with renting—especially over a longer horizon.

The Seasonal Factor

Jupiter’s seasonal rental demand (January through April) drives annual rent increases. Landlords often price long-term leases higher to offset missed seasonal income, which means renters face frequent hikes.

A fixed-rate mortgage, even with higher upfront costs, can feel more stable than renegotiating a lease every year.

The Impact of HOA Fees in Jupiter

Buying Power Reduction

HOA fees are unavoidable in many Jupiter communities. A helpful rule of thumb:

- $250/month HOA ≈ $50,000 reduction in buying power

- $500/month HOA ≈ $100,000 reduction in buying power

- $750/month HOA ≈ $150,000 reduction in buying power

This is why two buyers with the same income can afford very different homes depending on community fees.

Rent Inclusion

Renters benefit here. HOA fees in Jupiter are almost always paid by the landlord, meaning tenants enjoy pools, gyms, security, and landscaping without the risk of special assessments or rising association budgets.

Financial Comparison Table

| Cost Category | Renting (Avg 2/2 Condo) | Buying (Avg 2/2 Condo) |

|---|---|---|

| Monthly Payment | $2,800 – $3,500 | $3,800+ (Mortgage + HOA + Insurance) |

| Maintenance Liability | $0 | $300 – $500/month (reserves) |

| Insurance Cost | ~$25/month (renters) | $400 – $600/month (hazard & flood) |

| Equity Building | None | Principal paydown + appreciation |

Frequently Asked Questions

Is it a good time for a first-time home buyer in Florida in 2026?

It can be, but only with stable income, strong reserves, and a long-term plan. Insurance and HOA costs matter as much as price.

How much have Jupiter, FL, homeowners' insurance rates increased this year?

Rates vary widely by property type and location, but many owners are seeing noticeable annual increases, especially in coastal zones.

Are Abacoa rentals cheaper than buying a similar home in The Heights?

Often no. Abacoa rents tend to run higher due to demand, while ownership in The Heights may offer lower monthly overhead.

Do HOA fees in Jupiter typically cover roof repairs?

It depends on the association. Condo HOAs often cover roofs; townhome and single-family HOAs frequently do not.

Does the seasonal rental market affect long-term lease prices?

Yes. Seasonal demand pushes annual rents higher to compensate for peak-month pricing.

What is the minimum down payment required for a condo in Jupiter?

Typically 3–5% for qualified buyers, though some buildings require higher minimums.

Can I offset my mortgage by renting my home seasonally in Jupiter?

Possibly—but only in communities that allow short-term or seasonal rentals.

Key Takeaway: Timeframe Dictates Strategy

If you plan to stay less than five years, renting protects you from volatile insurance costs and steep closing expenses.

If you’re planting roots for the long haul, buying shields you from aggressive rent hikes driven by seasonal demand and allows you to lock in housing costs in a market that continues to attract long-term growth.

Every Jupiter neighborhood—and every buyer—runs on a different financial equation. If you’d like a personalized rent-versus-buy analysis based on your income, timeline, and target communities, let’s talk.

Call 561-744-8244 or email Realtor@jupiterflrealestate.com to get clear, no-pressure guidance from a local expert who knows the numbers behind the lifestyle.